Back to Insights

The proliferation of financial technology firms (fintechs) has been nothing short of explosive in recent years, particularly in Australia.

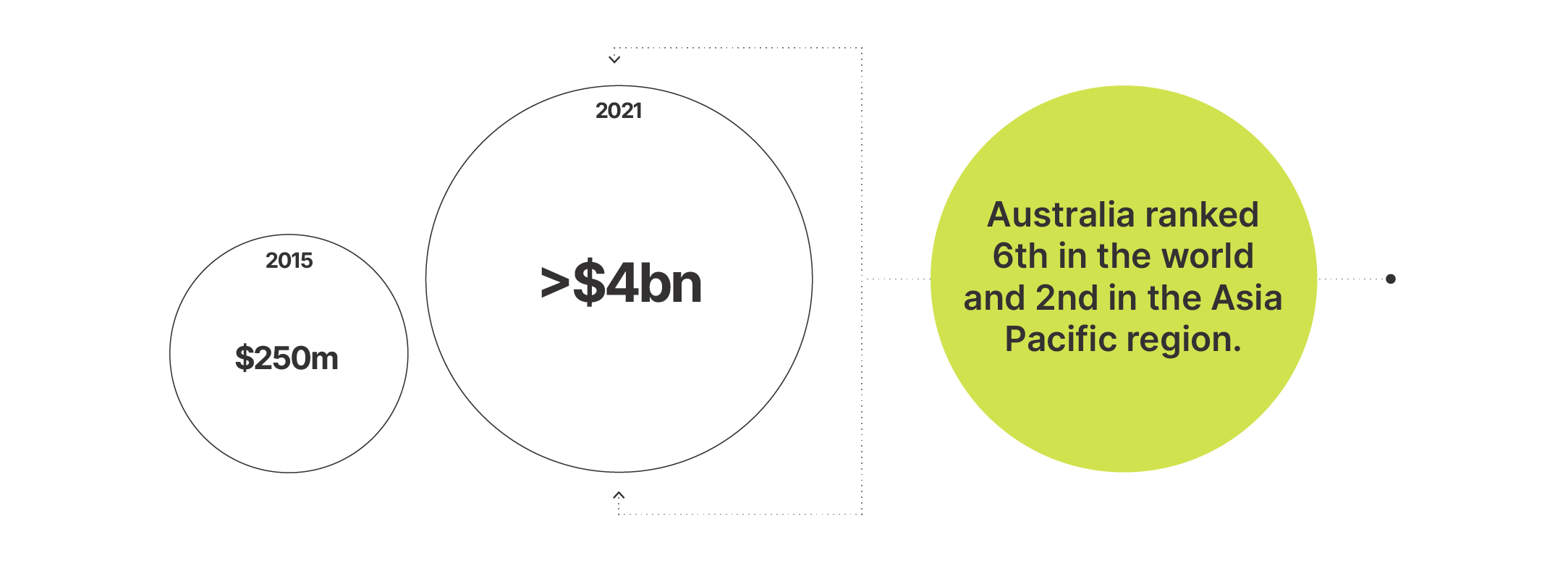

According to Fintech Australia, our local sector has grown from a $250m industry in 2015 to be worth more than $4 billion in 2021. And that sees Australia ranked 6th in the world and second in the Asia Pacific region, according to global research and analytics firm, Findexable.

There are likely a few factors helping us punch above our weight in this space:

- We have a stable and robust regulatory environment

- We have a deep talent pool and strong regional ties in Asia

- On the consumer side, Aussies are known for being amongst the fastest adopters of new technologies and we have also been one of the quickest to dump cash as a preferred payment method (we currently use cash for only 7% of purchases, and this is expected to drop to 2% by 2025).

But as buoyant and exciting as the fintech sector is, fintech businesses can prove very challenging for insurers, who view the sector as complex and high risk.

There a quite a few reasons for this.

Many fintechs are start-up businesses trialling innovative – but untested – propositions in the marketplace. New businesses have always had an alarmingly high rate of failure (some estimate a third of all new businesses fail in their first year) and its possible this is even higher for fintechs.

The financial services industry operates in a regulatory framework which is complex and rapidly evolving. And since the Hayne Royal Commission it’s been under even more scrutiny than ever before. If you described financial services as overregulated, you wouldn’t get too many people arguing with you. And existing regulation has struggled to keep pace with market developments such as crypto and buy-now-pay-later. All this complexity makes it easier to fall foul of the law, and that means increased risk.

On a related note, the entire sector has been in the cross hairs of the media and consumer advocate groups for a few years now, and whilst on the one hand the disruptors who eschew the ways of the traditional incumbents are welcomed as being more customer friendly, the honeymoon period can be short if there is even a sniff of poor consumer outcomes (think Afterpay).

And of course, there is the amount of sensitive data that financial services firms need to operate. That puts a big fat target on their back as far as cyber criminals are concerned, again raising the risk profile.

All these factors heighten the risk profile of fintechs from an insurance perspective, and when added to the existing challenges of limited supply in the Australian market (many global insurers are reducing their exposure to the sector and some have even withdrawn from the market altogether – for example AIG has recently announced it is exiting the financial services Professional Indemnity market in Australia), then accessing the most appropriate and robust insurance protection can be difficult.

Getting the right advice and right protection for fintechs needs specialised expertise. Headsure is a boutique insurance consultancy, and one of Australia’s foremost experts in providing advice and insurance solutions for businesses operating in complex environments. Our clients include some of the most innovative and well known fintechs in the market, as well as more traditional financial and professional services.

For an obligation free discussion about how we may be able to help your business, drop us a line.